Convergence rate

- 虽然optimization问题多用于基础研究,工程使用时有多种python库可供调用,但是了解其原理,一是有助于更好的选择optimization function,二是costumize自己的optimiation function(竞赛中常常用到)。

- 课程涉及大量推导,此处不分享相关slide.

- 首先看一下这篇https://zhuanlan.zhihu.com/p/27644403 ,对Convergence rate有一个大概的理解。

- 在发表optimization方向的论文时,需要尤其注意自己的模型属于哪种Convergence rate,并分析其表现: **_time and iteration count_**。

- 重点:Convergence rate only tells you how close each iteration gets to the best solution, however, it doesn't tell you how costly(timewise) each iteration is.**_ 解释一下就是,虽然有的optimization算法他Convergence rate很优秀,即可以几步就收敛到最优解,但是他每一次iteration的cost非常大,比如遍历整个数据集,或计算时间很长等,这就是trade-off,工程实现是需仔细考虑。

三种Convergence rate

-

Convergence rate:Sublinear < Linear < Quadratic (考)

- Sublinear:SGD (takes the amount of computations comparable with the total amount of the previous work.)

![]() (k是迭代次数,

(k是迭代次数,是k次迭代的risk值,Sublinear形式的特征是

在分母)

> Linear: GD (each new right digit of the answer takes a constant amount of computations)

![]() (Linear形式是k在指数)

(Linear形式是k在指数)

> Quadratic: 牛顿 (each iteration doubles the number of right digits in the answer,but expensive)

![]() (Quadratic形式)

(Quadratic形式)

(大家都用过的例子:SGD快,但是收敛效果不一定好,GD慢,但是遍历整个数据集,收敛效果好)

例如:你只是一个theoretician,不关心运行时间,你应该选择牛顿optimization,如果你是一个practitioner ,你应该选择DG或SGD。

optimization算法分析

(GD,SGD属于first order minimization,只保证收敛到stationary point, 而不保证收敛到local minima。)

GD----Linear convergence,以GD为例,讲解如何进行更好的optimization。

- 先我们希望需要去优化的loss function是strong convex并且smooth的(特别重要),基于这两个条件,可以证明GD算法属于linear convergence(证明见ppt19-21).(如果GD不可导,则需要使用subgradient代替gradient,此时推导过程基本不变)

- 如果只进行convex假设而不是strong convex,则GD的convergence rate只能退化成sublinear convergence rate,即正比于(1/t).

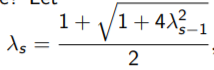

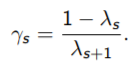

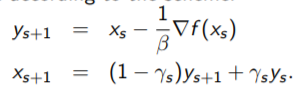

下面介绍如果并不满足strong convex假设,如何accelerate GD算法: Nesterov's Accelerated GD

- 思想: 每迈出一步,这一步的方向不光是当前的梯度方向,还要加一部分上一步得到的梯度。

- algorithm:(ppt-26)

Step1:

Step2: init:![]()

Step3:

(第一行和GD完全一样,第二行加入了上一次的direction)

- torch.optim.SGD(params, lr=, momentum=0, dampening=0, weight_decay=0, nesterov=False)中使用这个参数,即在发现optimization funcction的convex性不是很好时将nesterov=False置为true,可得到1/t^2的convergence rate,虽然也是sublinear,但是比不加好很多。

- 源码阅读

- 如果从另一种证明方法得知,convergence rate反比与objective function的hessian矩阵的condition number,即smooth/convex。(strong vonvex:Q,convex: 根号Q),Q越小,收敛越快。)

(各大library不太会使用GD做优化器,但是GD方便手写,且是基础中的基础,和SGD是相同的,上面的方法在SGD中就用的很多了)

SGD----Sublinear

- 证明略。

- 如果objective function是strong convex的,convergence rate可证明:正比于log(t)。

因为strong convex代表了slope更加steep,自然下降的更快。

(注意,GD的的步长一般认为是固定值(也有变化的),但是SGD的步长一般认为是变化的,到后面越来越慢![]() ,其中B是参数w的外界

,其中B是参数w的外界,

是当前vector的外界)。

- 步长: theoreticians 只证明SGD收敛可行,practitioners需要真正实现他,所以各个不同的Library都有自己的步长自适应算法,例如torch采用的Adagrad,RMSprop等,try to make two communities more agree with each other.

Newton method

虽然convergence rate很好,但是每次迭代expensive,因为要计算hessian矩阵的逆。

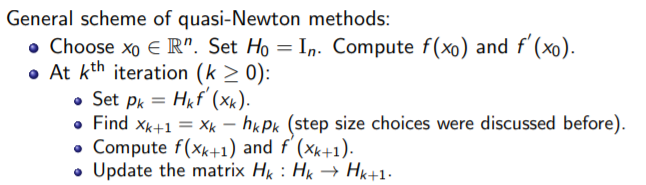

Quasi-Newton methods

因为first order的算法虽然convergence rate不太优秀,但是一次iteration计算资源消费较少,牛顿法则相反。所以提出了拟牛顿法这种改进。super-linear

首先,first order算法的迭代更新是

它满足approximation of the function f (x):(f(x)的一阶泰勒展开)

这个方程求极小值。(对他求一阶导,使一阶导为0)

同样,Newton methods迭代规则是:

![]()

它满足approximation of the function f (x):(二阶泰勒展开)

求极小值。

所以:Can we construct better approximations that φ1(x), but less expensive than φ2(x)?

它就是![]()

于是,f''(x)被替换成了G。

算法是:(H就是G-1)

如何更新H呢:

- BFGS

但是这样就会每次要存储一个n*n的矩阵,是昂贵的。

- LBFGS(减小存储空间)

于是,只要存V这个矩阵就行了,前k个特征值被记录在S中。

-1的计算也给常快速:

![]()

最后放上使用SciPy库的代码(homework)

BFGS,LBFGS

The code was inspired by https://nbviewer.jupyter.org/github/fabianp/pytron/blob/master/doc/benchmark_logistic.ipynb

import numpy as np

import torch

import torch.nn as nn

import scipy.io as scio

from sklearn.gaussian_process import kernels

from tqdm import tqdm, trange

import scipy.stats as st

import torch

import numpy as np

from tqdm import tqdm, trange

import torch.nn.functional as F

import torch.nn as nn

from scipy.stats import logistic

import matplotlib.pyplot as plt

from torch.utils.data import TensorDataset, DataLoader, RandomSampler, SequentialSampler

from sklearn.model_selection import train_test_split

import matplotlib.pyplot as plt

from sklearn import metrics

from sklearn.linear_model import LogisticRegression

from scipy.optimize import minimize

from scipy import optimize

import numpy as np

from scipy import linalg, optimize

#

The code was inspired by https://nbviewer.jupyter.org/github/fabianp/pytron/blob/master/doc/benchmark_logistic.ipynb

def phi(t):

# logistic function

idx = t > 0

out = np.empty(t.size, dtype=np.float)

out[idx] = 1. / (1 + np.exp(-t[idx]))

exp_t = np.exp(t[~idx])

out[~idx] = exp_t / (1. + exp_t)

return out

def grad_hess(w, X, y, alpha):

# gradient AND hessian of the logistic

z = X.dot(w)

z = phi(y * z)

z0 = (z - 1) * y

grad = X.T.dot(z0) + alpha * w

def Hs(s):

d = z * (1 - z)

wa = d * X.dot(s)

return X.T.dot(wa) + alpha * s

return grad, Hs

def loss(w, X, y, alpha):

# loss function to be optimized, it's the logistic loss

z = X.dot(w)

yz = y * z

idx = yz > 0

out = np.zeros_like(yz)

out[idx] = np.log(1 + np.exp(-yz[idx]))

out[~idx] = (-yz[~idx] + np.log(1 + np.exp(yz[~idx])))

out = out.sum() + .5 * alpha * w.dot(w)

return out

def gradient(w, X, y, alpha):

# gradient of the logistic loss

z = X.dot(w)

z = phi(y * z)

z0 = (z - 1) * y

grad = X.T.dot(z0) + alpha * w

return grad

c = []

H= []

loss_ = []

res = []

for i in range(3):

data = scio.loadmat("data1.mat")

tr_x = np.asarray(data["TrainingX"])

tr_y = np.asarray(data["TrainingY"])

D = np.column_stack((tr_x, tr_y))

D1 = D[0:5000, :]

np.random.shuffle(D1)

D1 = D1[0:2000, :]

D2 = D[5000:, :]

np.random.shuffle(D2)

D2 = D2[0:2000, :]

train_xx = np.row_stack((D1[:, 0:784], D2[:, 0:784]))

train_y = np.row_stack((D1[:, 784:], D2[:, 784:]))

train_y = [arr[0] for arr in train_y]

print(np.shape(train_y))

train_x = metrics.pairwise.rbf_kernel(train_xx, train_xx)

m, n = np.shape(train_x)

te_x = np.asarray(data["TestX"])

test_y = np.asarray(data["TestY"])

test_x = metrics.pairwise.rbf_kernel(te_x, train_xx)

w = np.random.random((1, n))

alpha = 1.

X = train_x

y = train_y

print('BFGS')

timings_bfgs = []

precision_bfgs = []

w0 = np.zeros(X.shape[1])

def callback(x0):

prec = linalg.norm(gradient(x0, X, y, alpha), np.inf)

precision_bfgs.append(prec)

l = loss(x0,X, y, alpha)

loss_.append(l)

ht = np.dot(test_x, x0)

ht = phi(ht)

count = 0

for i in range(np.shape(ht)[0]):

if (ht[i] > 0.5):

s = 1

else:

s = -1

if (s != test_y[i]):

count = count + 1

c.append(count / 1000.)

print(count / 1000.)

_,K= grad_hess(x0,X, y, alpha)

H.append(K)

callback(w0)

out = optimize.fmin_bfgs(loss, w0, fprime=gradient,

args=(X, y, alpha), gtol=1e-10, maxiter=100,

callback=callback)

最后

以上就是舒适刺猬最近收集整理的关于机器学习中optimization问题 Convergence rate optimization算法分析的全部内容,更多相关机器学习中optimization问题内容请搜索靠谱客的其他文章。

发表评论 取消回复